When to get STR insurance is one of the most expensive questions hosts get wrong. Scrambling for coverage three days before your first guest leads to inadequate policies, rush premiums, and delayed launches.

When to get STR insurance is the single biggest timing decision new investors face — and most get it wrong. One of the most common mistakes new short-term rental investors make is treating insurance as an afterthought. They spend months analyzing markets, negotiating the purchase price, designing the perfect interior, and building their listing — only to scramble for insurance three days before their first guest arrives.

This reactive approach is incredibly dangerous. The STR insurance market is complex, and securing the right commercial policy takes time. Waiting until the last minute often results in hosts settling for inadequate coverage, paying exorbitant rush-bound premiums, or delaying their launch because they cannot secure a policy in time.

To ensure your investment is protected from day one and your launch goes smoothly, you must integrate insurance into your property acquisition timeline. In this guide, we provide a step-by-step framework for when to get STR insurance, detailing exactly what to do at each stage.

Your insurance strategy should begin before you even identify a specific property. The location and features of a home drastically impact insurability and premium cost.

Analyze Environmental Risks. Is the property in a high-wildfire-risk area? A coastal hurricane zone? A FEMA Special Flood Hazard Area? Check the property’s flood zone for free at FEMA’s Flood Map Service Center.

Identify High-Risk Amenities. Pool, hot tub, trampoline, private dock, multi-level balcony — these require higher liability limits.

Get Preliminary Estimates. Contact an STR-specialized broker for a ballpark premium. A property profitable at $1,200/year in insurance may not pencil at $4,500/year.

Understand Regulations. Research STR regulations in your target market. Permit + insurance requirements affect ROI.

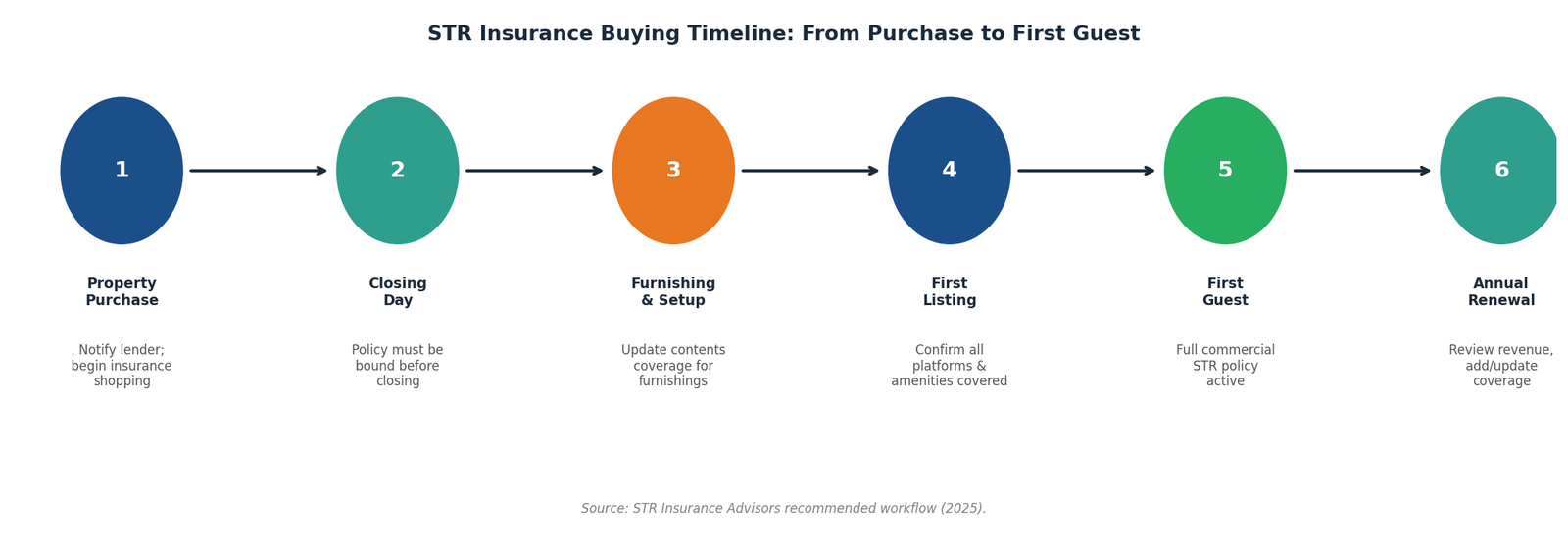

The moment your offer is accepted and you enter escrow, the clock is ticking. Your lender requires proof of insurance (a “binder”) before clearing the loan to close.

Notify Your Lender of the STR Intent. Some lenders require a commercial policy for STRs; others accept homeowners. Know their requirements before shopping.

Engage a Specialized STR Broker. Do not call your standard auto/home agent. Contact a commercial STR specialist with direct carrier relationships.

Provide the broker with: property address and square footage, year built and construction type, complete list of amenities, estimated annual revenue, intended booking platforms.

Address the Vacant Property Issue. If you plan to renovate or furnish for several weeks before hosting, you may need a “Builder’s Risk” or “Vacant Property” endorsement.

Shop Multiple Carriers. The STR insurance market has grown significantly. Compare quotes — meaningful price differences exist.

You cannot close on a financed property without insurance in place.

Bind the Policy. Your commercial STR policy must be active on the exact day you take ownership. No grace period — if a fire breaks out on closing day and your policy starts tomorrow, you have no coverage.

Review the Declaration Page. Ensure: Named Insured correct (your name or LLC), property address correct, liability limits match agreement, Replacement Cost Value accurate, effective date is closing date.

Confirm Lender as Additional Insured. Your mortgage lender will require listing as “Mortgagee.” Verify your broker handled this.

Once you own the property, you will spend weeks buying furniture, installing tech, and staging for photos.

Track Every Expense with Receipts. Store all furniture and electronics receipts in the cloud. If a fire destroys the property the day before launch, you need these to file a contents claim.

Update Your Contents Limit. If you end up spending $45K on furnishings instead of estimated $20K, call your broker immediately to increase coverage.

Install Safety and Monitoring Technology. Before first guest: smart water leak sensors, connected smoke/CO detectors, smart locks, noise monitor (Minut/NoiseAware), security cameras.

Create a Property Inventory. Conduct a room-by-room video walkthrough of the fully furnished property. Store in cloud.

Before you hit “Publish” on Airbnb or Vrbo, do a final insurance review.

Verify Multi-Channel Coverage. Confirm coverage applies to Airbnb, Vrbo, Booking.com, and direct bookings.

Review House Rules for Compliance. Examples: “No open flames on wooden decks,” “Pool gate must remain locked,” “Maximum X guests.” Reflect insurance requirements in house rules.

Obtain Your Certificate of Insurance (COI). If your municipality requires proof of commercial liability for permits, submit COI to the city. Do not launch without your permit.

Notify Your Broker of Launch Date. Some carriers require notification when property transitions from setup to active rental.

Once your STR is live, insurance becomes ongoing operational responsibility.

Report Claims Promptly. Most policies require prompt notification — delaying can result in denial.

Document Every Incident. Even minor incidents not rising to a claim. If a guest later files suit, this documentation is critical.

Update Your Policy for New Amenities. Adding a hot tub, fire pit, or pool? Notify your carrier immediately. Failing to disclose can void coverage.

Insurance is not “set it and forget it.” As your business grows, your needs evolve.

Review Your Revenue. Did your property gross $90K instead of projected $60K? Increase your “Loss of Business Income” limit to match actual revenue.

Update Replacement Cost Value. Construction costs increase. Ask your broker to run a replacement cost estimator at each renewal.

Re-Shop the Market. Rates fluctuate, new carriers enter the market. Compare your renewal against alternatives.

Review Your Liability Limits. If net worth has grown, increase umbrella coverage accordingly.

Securing the right STR insurance requires foresight, planning, and ongoing attention. By integrating insurance into your acquisition timeline — starting before you make an offer — you avoid last-minute scrambles.

For deeper context, read our companion guides on STR insurance tax deduction and STR risk management with LLCs.

STR Insurance Advisors builds a customized insurance strategy that scales with your business — from property search through annual renewal.