STR insurance tax deduction is one of the most overlooked profit-protection tools in the vacation rental business. Your full commercial premium is deductible — and the after-tax cost of proper coverage is far lower than you think.

STR insurance tax deduction strategy starts with one simple truth: commercial insurance is not just a shield against liability — it is a fully deductible business expense that actively reduces your tax burden. When you factor in the tax savings, the true cost of proper commercial coverage is significantly lower than the sticker price suggests.

Many hosts hesitate to upgrade from a cheap, inadequate homeowners policy to a robust commercial STR policy because of the higher premium. They fail to realize that the IRS rewards you for buying real protection.

In this guide, we explore the IRS rules regarding STR insurance tax deduction strategy, how to properly report your premiums, the critical 14-Day Rule, and why investing in commercial coverage is smart financial planning on both ends of the ledger.

The Internal Revenue Service is very clear regarding the expenses associated with operating a rental property. According to IRS Publication 527 (Residential Rental Property), you can deduct the ordinary and necessary expenses for managing, conserving, and maintaining your rental property.

Insurance premiums fall squarely into this category. The IRS explicitly lists “insurance” as a deductible rental expense, and this applies to virtually every type of insurance policy directly related to your rental activity.

As a short-term rental host, your STR insurance tax deduction can include premiums you pay for:

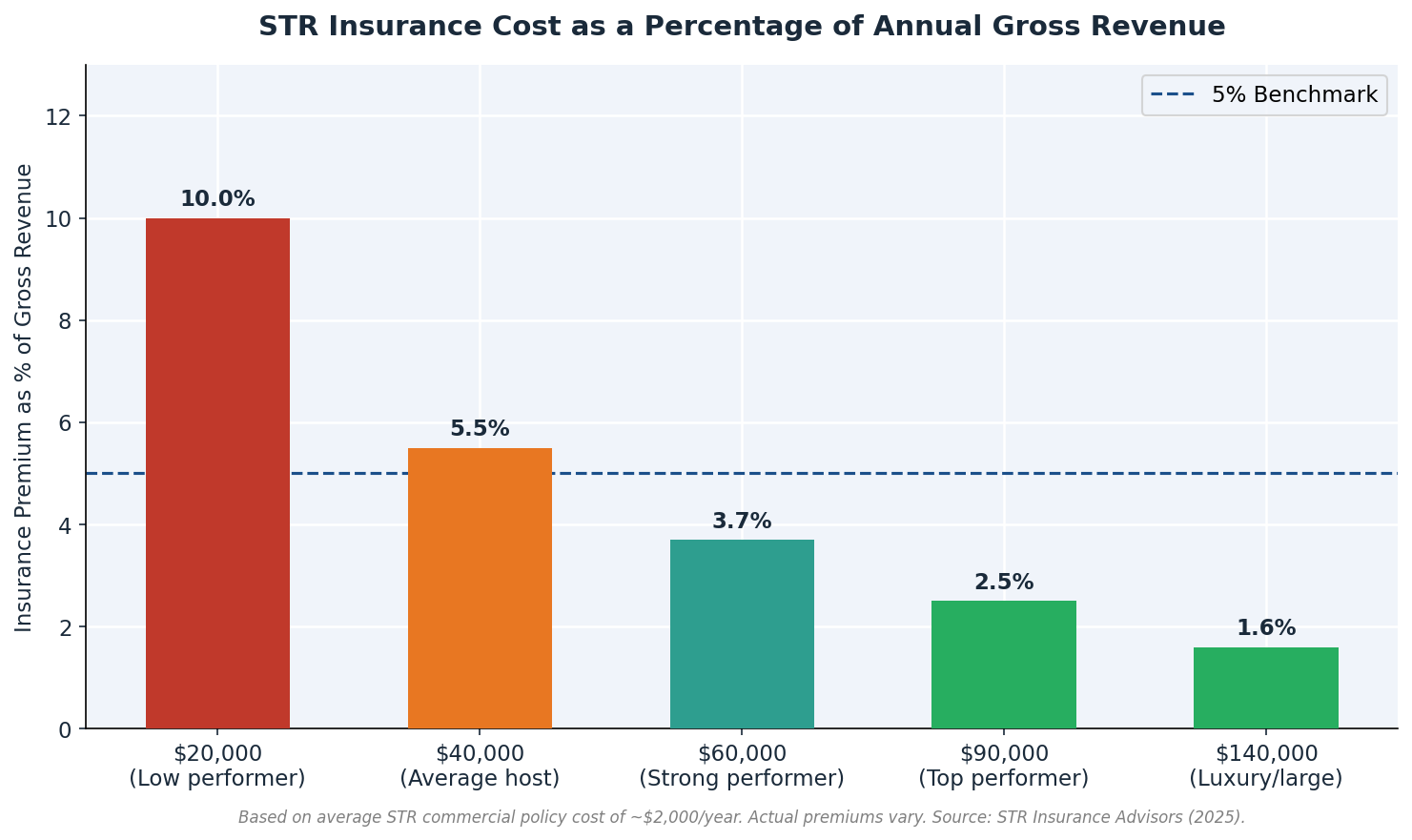

If you pay $3,500 annually for a comprehensive commercial STR policy, that entire $3,500 is typically deductible from your gross rental income.

| Scenario | Gross Revenue | Premium | Tax Saved |

|---|---|---|---|

| Host A (24% bracket) | $60,000 | $2,800 | $672 |

| Host B (32% bracket) | $120,000 | $4,200 | $1,344 |

| Host C (37% bracket) | $250,000 | $6,500 | $2,405 |

For Host C, a $6,500 commercial premium effectively costs only $4,095 after the federal STR insurance tax deduction. Add state income tax savings and the effective cost drops further.

The IRS rules become more complex if you use the STR property for personal vacations in addition to renting it out. The IRS categorizes properties based on how many days they are rented versus how many days they are used personally.

If you rent your property for fewer than 15 days during the year and use it personally for 15 days or more, the IRS considers it a personal residence under Section 280A. You do not have to report the rental income.

However, you cannot deduct rental expenses, including your insurance premium, as rental business expenses. You may still deduct mortgage interest and property taxes as personal itemized deductions on Schedule A.

If you rent the property for 15+ days and use it personally for more than 14 days (or 10% of rental days, whichever is greater), it is a “mixed-use” property.

You must allocate your expenses — including insurance — between personal and rental use.

The Allocation Formula:

Example: You rent 200 days, use personally 50 days. Rental use = 200 ÷ 250 = 80%. If premium is $3,000, you deduct $2,400.

If you never use the property personally, you can deduct 100% of your insurance premium. This is the simplest scenario and the most common for professional STR investors.

How you report your income depends on the level of services you provide and how the IRS classifies your STR activity.

The vast majority of STR hosts report on IRS Schedule E. There is a specific line item for “Insurance” where you list your deductible premium.

Schedule E reporting is appropriate when you provide the property for guests without substantial services. The key benefit is that net rental income is not subject to self-employment taxes (15.3%).

If you provide “substantial services” like daily maid service, daily breakfast, or concierge service, the IRS may classify your STR as an active business. You report on Schedule C.

The downside: net income becomes subject to self-employment taxes. Most STR hosts deliberately avoid hotel-like services to maintain Schedule E treatment.

If the average rental period for your property is 7 days or fewer, the IRS does not automatically classify it as passive under Section 469. Consult a CPA who specializes in real estate taxation.

The most significant tax benefit of owning a rental property is depreciation — the ability to deduct the cost of the building over 27.5 years for residential rental property.

For a $500,000 property excluding land, the annual depreciation deduction is approximately $18,182 per year. This depreciation is the primary reason real estate investors can show a tax loss on paper while generating positive cash flow.

The Insurance-Depreciation Connection: If your property is destroyed and your homeowners insurance denies the claim because you were operating an STR, you lose the asset, the income, and the massive depreciation deduction — all at once.

A commercial STR policy ensures that if a covered peril destroys your property, you receive full Replacement Cost Value to rebuild. This protects not just the physical asset, but the entire tax and income-generating structure built around it.

To properly claim your STR insurance tax deduction, follow these steps.

Step 1: Keep All Premium Invoices. Maintain copies of every insurance premium invoice or statement. Your insurance company will provide an annual summary.

Step 2: Separate Personal and Rental Policies. Keep your homeowners and commercial STR policies completely separate. Never commingle expenses.

Step 3: Calculate Your Allocation (If Mixed-Use). Apply your rental use percentage to your annual premium to determine the deductible amount.

Step 4: Report on Schedule E, Line 9. Line 9 is specifically designated for “Insurance.” Enter your deductible premium amount here.

Step 5: Consult a CPA. Work with a CPA who specializes in real estate taxation to ensure you are maximizing your deductions.

Securing the right commercial STR insurance is not just about risk management — it is a smart financial strategy that reduces your tax burden while protecting your most valuable assets.

For deeper context, read our companion guides on the true cost of being uninsured and risk management with LLCs and umbrella policies.

STR Insurance Advisors structures commercial policies that protect your asset and your tax position simultaneously.