STR insurance requirements by city have tripled in 5 years. Over 430 U.S. cities now mandate commercial liability coverage for STR permits — and AirCover does not qualify.

STR insurance requirements by city have become the single biggest compliance challenge facing vacation rental hosts. The “Wild West” era of the short-term rental industry is officially over. Across the United States, municipalities, counties, and state governments are implementing strict zoning laws, permit quotas, safety inspections, and operational mandates.

While much of the public debate focuses on density caps and primary residence requirements, there is a massive, often overlooked component: mandatory commercial insurance requirements. Governments are forcing hosts to carry robust commercial liability policies as a prerequisite for obtaining an operating permit.

In this guide, we explore how STR insurance requirements by city are reshaping the industry, which markets have the most stringent requirements, why platform guarantees cannot satisfy these mandates, and what you need to do to remain compliant.

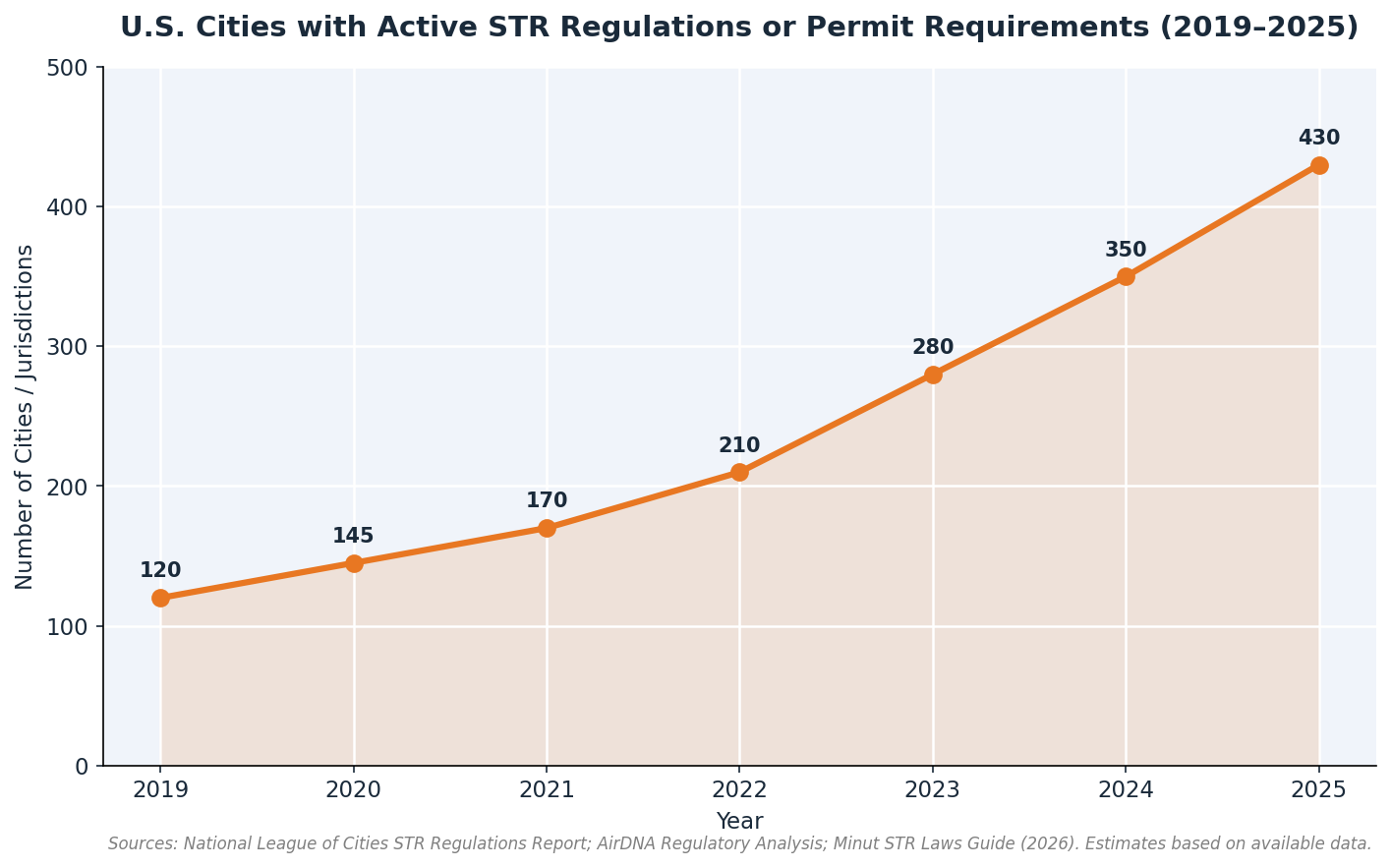

The pace of STR regulation is accelerating at a remarkable rate. According to National League of Cities data, the number of U.S. cities with active STR regulations has more than tripled since 2019, growing from roughly 120 cities to over 430 by 2025.

This regulatory wave is driven by housing affordability concerns, neighborhood quality of life complaints, high-profile liability incidents, and tax revenue optimization.

The most common insurance requirement emerging in new STR ordinances is the mandate for $1,000,000 in Commercial General Liability (CGL) coverage.

Massachusetts: Under Chapter 64G, Section 6B, all operators must maintain at least $1,000,000 in liability insurance.

Vermont: Act 48 (2024) requires STR operators to register with the state and carry commercial liability insurance.

Hawaii: All counties require proof of commercial liability insurance as part of the permit application process. Maui County has implemented some of the strictest STR regulations in the country.

| Market | Insurance Required | Permit |

|---|---|---|

| New York City, NY | $1M CGL | Yes (Local Law 18) |

| San Francisco, CA | $500K liability | Yes |

| Austin, TX | Commercial liability | Yes |

| Nashville, TN | $1M CGL | Yes |

| Denver, CO | $1M CGL | Yes |

| Chicago, IL | $1M CGL | Yes |

| Miami Beach, FL | $1M CGL | Yes |

| Scottsdale, AZ | $500K liability | Yes |

| Honolulu, HI | $1M CGL | Yes |

| Portland, OR | $1M CGL | Yes |

Local governments are universally rejecting platform guarantees as proof of insurance.

It is Not an Insurance Policy: AirCover is a “Host Guarantee,” not a primary insurance policy. It does not provide a Certificate of Insurance (COI) listing the host as Named Insured — which is exactly what permit offices require.

It Only Covers Platform Bookings: Local mandates require coverage 24/7/365. AirCover provides zero coverage during periods between bookings, during direct-booking stays, or when a cleaner is on the property.

It Cannot Be Verified by Third Parties: Insurance certificates are issued by licensed carriers and can be independently verified. AirCover is a contractual promise that Airbnb can modify or revoke.

Operating an STR without required permits and insurance can destroy your business overnight.

Massive Daily Fines: In NYC, operating illegally results in $1,000–$5,000 per day fines. San Francisco can reach $484 per day.

Platform Delisting: NYC Local Law 18 resulted in over 15,000 listings removed from Airbnb in 2023. Hosts lost $50K–$100K in annual revenue overnight.

Total Personal Liability Exposure: If you operate illegally and a guest is severely injured, your homeowners insurance will deny the claim, leaving you personally liable.

If you operate in a regulated market, proactively upgrade your insurance.

Step 1: Read the Ordinance. Read the actual text. Look for the “Insurance Requirements” section.

Step 2: Check for Specific Policy Language. Some cities require explicit mention of “short-term rental activity.”

Step 3: Request a Certificate of Insurance (COI). This one-page document is exactly what permit offices need.

Step 4: Renew Your Permit Annually. Proof of current insurance is typically required at each renewal.

Step 5: Partner with a Specialized STR Broker. We track regulatory changes nationally and structure policies that meet local requirements.

The era of flying under the radar is over. Compliance is no longer optional — it is the cost of entry. Mandatory commercial insurance requirements are becoming the norm.

For deeper context, read our companion guides on Florida vacation rental insurance and STR risk management with LLCs.

STR Insurance Advisors tracks regulations across the country and structures policies guaranteed to meet local municipal requirements.