Florida vacation rental insurance is the highest-stakes coverage decision a coastal STR host can make. Beachfront properties earn $100K–$300K+ a year, but hurricane deductibles, flood gaps, and pool liability can wipe out an entire season in a single storm.

Florida vacation rental insurance sits at the center of the most volatile property insurance market in the United States. The state is the undisputed king of the U.S. vacation rental market — in 2024 alone, Florida welcomed 143 million visitors, with millions flocking to coastal short-term rentals from the Panhandle to the Keys.

For property owners, the financial rewards are immense. Beachfront properties in markets like Destin, 30A, and the Florida Keys routinely generate $100,000 to $300,000 or more in annual gross revenue.

However, operating a vacation rental in the Sunshine State comes with a unique, highly volatile set of risks that standard insurance policies simply cannot handle. Skyrocketing premiums, hurricane threats, pool and beach liability, and a rapidly evolving regulatory landscape mean Florida STR hosts face an insurance environment unlike anywhere else in the country.

In this guide, we break down exactly what Florida vacation rental insurance must include to protect your coastal investment in 2026 and beyond.

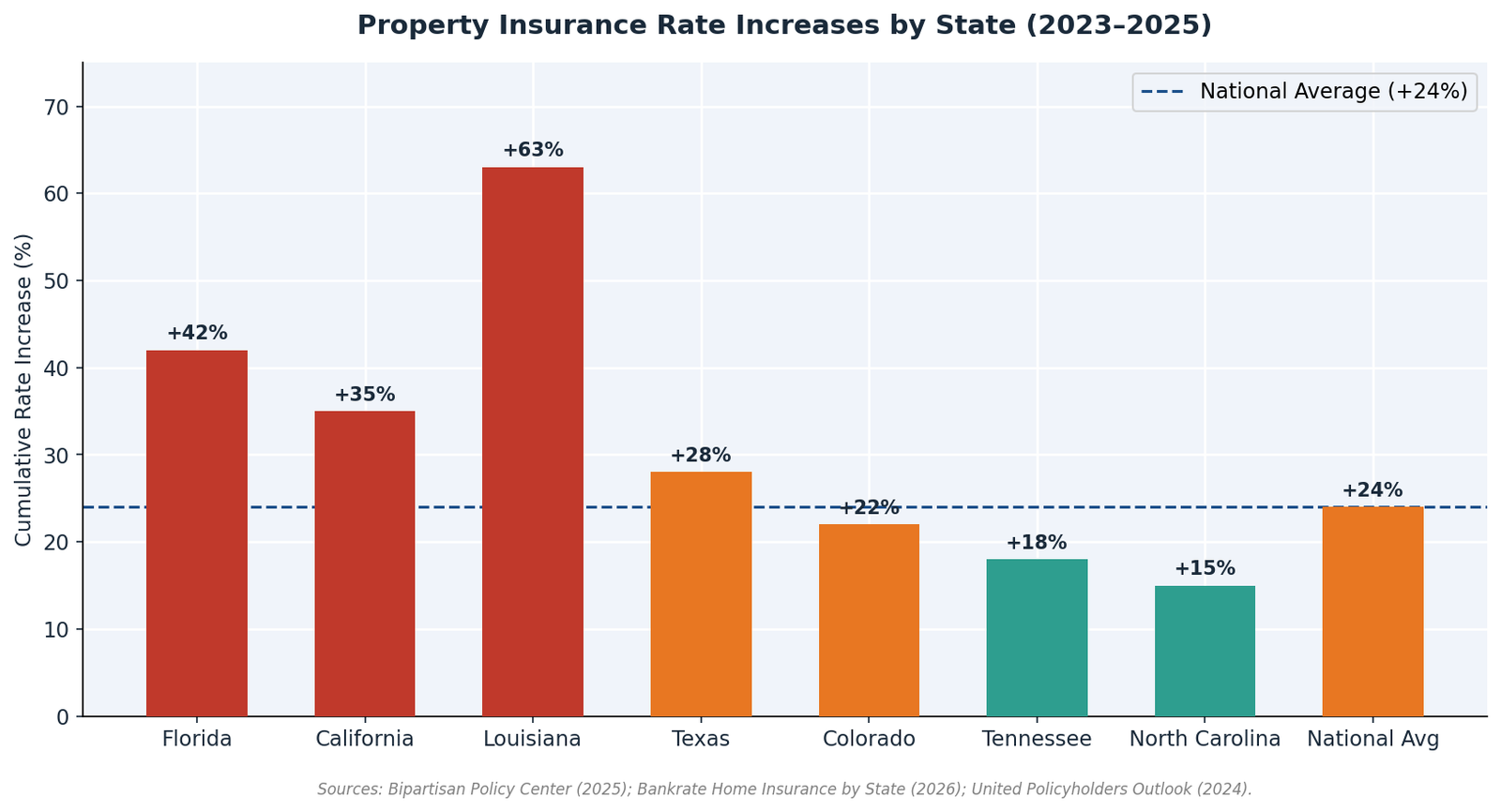

Before diving into specific coverages, it is crucial to understand the macro environment of Florida property insurance. The market has been in a state of crisis for several years, and the situation directly impacts every STR owner in the state.

According to the Bipartisan Policy Center, homeowners insurance rates have increased by an average of 24% nationally over the past two years. In Florida, however, the increases have been far more severe.

Some coastal property owners have seen premiums double or triple. The Insurance Information Institute reports that the average Florida homeowner now pays over $6,000 per year for property insurance — more than triple the national average of approximately $1,900.

For commercial STR properties, which carry higher risk profiles than owner-occupied homes, the premium increases have been even more dramatic. Coastal STR owners in Miami Beach, Fort Lauderdale, and the Florida Keys have seen commercial Florida vacation rental insurance premiums jump 50% to 100% in a single renewal cycle.

Due to the high frequency of severe weather events and a history of rampant litigation related to roofing claims, several major national carriers have either stopped writing new policies in Florida or exited the state entirely.

Farmers Insurance, Bankers Insurance, and several other carriers have announced significant pullbacks from the Florida market since 2022.

As a result, many STR owners are forced to turn to Citizens Property Insurance Corporation (the state-backed insurer of last resort) or “Surplus Lines” carriers.

Surplus lines carriers are not backed by the state guaranty fund, but they specialize in high-risk properties and are often the only option for commercial short-term rentals located directly on the coast. Working with a specialized STR broker is essential to navigating this complex Florida vacation rental insurance market.

The 2022 and 2023 hurricane seasons were particularly devastating for Florida property owners. Hurricane Ian (2022) caused an estimated $112 billion in damage, making it one of the costliest hurricanes in U.S. history.

The storm destroyed thousands of vacation rental properties in the Fort Myers and Cape Coral area. Many hosts discovered — too late — that their policies had inadequate limits, high hurricane deductibles, or excluded certain types of damage.

The lessons from Ian are clear: Florida STR owners must treat hurricane preparation as a year-round priority, not just a seasonal concern. Solid Florida vacation rental insurance is the foundation of that preparation.

If you are renting your Florida property on Airbnb, Vrbo, or through a direct booking site, a standard homeowners policy is entirely inadequate. The Insurance Information Institute classifies STR activity as a commercial exposure, meaning standard policies will likely deny claims arising from guest activities.

To properly protect a Florida STR, you need a purpose-built Commercial Short-Term Rental Policy containing five core elements.

In Florida, windstorm coverage is the most critical and often the most expensive component of your policy. Understanding how vacation rental hurricane coverage deductibles work is essential for every coastal property owner.

The Hurricane Deductible: Unlike standard perils (like fire or theft) which typically have a flat dollar deductible (e.g., $2,500), hurricane deductibles in Florida are usually calculated as a percentage of the dwelling’s insured value — typically 2%, 5%, or even 10%.

Example: If your beachfront home is insured for $1,000,000 and you have a 5% hurricane deductible, you are responsible for the first $50,000 of damage out of pocket before the insurance kicks in. For a $2 million property with a 5% hurricane deductible, your out-of-pocket exposure is $100,000.

What Triggers the Hurricane Deductible: The hurricane deductible is typically triggered when the National Hurricane Center issues a hurricane watch or warning for your area. This means that even if your property sustains significant wind damage from a tropical storm (not a named hurricane), the standard deductible — not the hurricane deductible — applies. Know your policy’s specific trigger language.

Windstorm Exclusions: Some commercial policies in Florida exclude windstorm entirely, requiring you to purchase a separate wind-only policy through Citizens or a private windstorm carrier. This is particularly common for properties located in coastal high-hazard areas (Zone A or Zone V on FEMA flood maps). Always verify whether your Florida vacation rental insurance includes windstorm or whether you need a separate policy.

A standard commercial STR policy does not cover flood damage. In Florida, storm surge from a hurricane or heavy torrential rain is a massive risk.

According to FEMA, just one inch of floodwater can cause over $25,000 in damage to a home. Florida flood insurance STR coverage is therefore not optional.

You must purchase a separate flood insurance policy, either through the National Flood Insurance Program (NFIP) or a private flood insurer. Private flood insurance is becoming increasingly popular for luxury STRs because the NFIP caps dwelling coverage at $250,000, which is vastly insufficient for most coastal vacation homes.

Private flood policies often offer “Loss of Use” coverage — reimbursing you for lost rental income while the property is being repaired — which the NFIP does not provide.

| Feature | NFIP Flood Policy | Private Flood Insurance |

|---|---|---|

| Maximum Dwelling Coverage | $250,000 | Unlimited (based on home value) |

| Maximum Contents Coverage | $100,000 | Unlimited |

| Loss of Use / Business Income | Not available | Available |

| Replacement Cost Value | ACV only | Available |

| Waiting Period | 30 days | 14 days (some carriers) |

| Premium | Government-set | Market-based |

For any Florida STR with a replacement cost value exceeding $250,000 — which includes virtually every coastal vacation rental — private flood insurance is the superior option.

Florida STRs are prized for their amenities — specifically, swimming pools, hot tubs, and multi-level balconies overlooking the water. These amenities are also the primary drivers of liability claims, which is why Florida pool liability insurance is a non-negotiable layer of any Florida vacation rental insurance plan.

A commercial STR policy should provide $1 million to $2 million in Commercial General Liability (CGL) coverage. You must verify that your policy does not contain sublimits or exclusions for swimming pools.

If a guest slips on a wet pool deck and suffers a traumatic brain injury, you need the full weight of a $2 million commercial liability limit to cover the legal defense and settlement costs.

Beach Access Liability: If your property provides private beach access, you may face additional liability exposure for injuries occurring on the beach path or at the water’s edge. Confirm that your CGL policy covers injuries occurring on all areas of the property, including beach access paths and dune walkovers.

Pool Safety Compliance: Florida law requires all residential swimming pools to have specific safety features, including pool barriers (fences), self-closing gates, and pool alarms. Failure to comply with Florida’s Pool Safety Act (Section 515.27, Florida Statutes) can expose you to negligence claims if a guest or child is injured in the pool.

If a Category 4 hurricane damages your property and renders it uninhabitable for six months during the peak winter season, the physical damage is only half the financial disaster.

The lost rental revenue can easily bankrupt a host who relies on that income to pay the mortgage. A proper commercial policy includes “Actual Loss Sustained” coverage.

This reimburses you for the rental income you would have earned while the property is being rebuilt, based on your historical booking data and future reservations. For a Florida coastal property generating $200,000 per year, a six-month outage means $100,000 in lost income. Ensure your Florida vacation rental insurance Loss of Business Income limit is sized to your actual revenue.

After a major hurricane, Florida’s building codes often require significant upgrades before a damaged structure can be rebuilt.

For example, if your 1980s-era beach house is 60% destroyed by a hurricane, local codes may require you to rebuild the entire structure to current standards — including impact-resistant windows, updated electrical systems, and elevated foundations. These upgrades can cost tens of thousands of dollars beyond the basic reconstruction cost.

Standard policies pay to rebuild the home to its pre-loss condition. Ordinance or Law coverage pays the additional cost of bringing the rebuilt structure up to current code. This coverage is essential for any Florida property built before 2002, when Florida adopted its current statewide building code.

Florida state law preempts local governments from banning short-term rentals entirely, but local municipalities have wide latitude to regulate them. Understanding the regulatory landscape is critical for maintaining your operating license and your Florida vacation rental insurance coverage.

Miami Beach: One of the most restrictive STR markets in Florida. Miami Beach has implemented strict zoning laws limiting STRs to specific districts and requiring annual permits with proof of commercial liability insurance.

Fort Lauderdale: Requires STR registration and has implemented noise ordinances and occupancy limits. Proof of insurance is required for permit renewal.

Orlando/Kissimmee: The gateway to Disney World has a massive STR market. Osceola County requires STR licenses and has implemented specific safety inspection requirements.

The Florida Keys: Monroe County has implemented some of the strictest STR regulations in the state, including permit caps and mandatory inspections. Insurance requirements are embedded in the permit process.

State Tax Requirements: Florida requires STR operators to collect and remit the Florida Transient Rental Tax (6%) and a local discretionary sales surtax (which varies by county, typically 0.5%–1.5%). Failure to collect and remit these taxes can result in significant fines and penalties. See the Florida Department of Revenue for current tax guidance.

Owning a vacation rental in Florida is a high-risk, high-reward endeavor. The combination of severe weather threats, a volatile insurance market, and the inherent liability of transient guests requires a sophisticated risk management strategy.

Do not rely on platform guarantees like AirCover, and do not attempt to hide your STR activity under a standard homeowners policy. Proper Florida vacation rental insurance is the only path that actually protects your coastal asset.

For deeper context, read our companion guides on the true cost of being uninsured, how STR regulations are changing insurance requirements, and luxury vacation rental insurance for high-value properties.

Work with a specialized broker at STR Insurance Advisors to navigate the complex Florida market, secure robust wind and flood coverage, and protect your coastal asset with a true commercial policy.

STR Insurance Advisors has direct relationships with carriers writing coastal commercial policies — wind, flood, pool liability, and loss of business income, structured for the Florida market.