Luxury vacation rental insurance is fundamentally different from standard STR coverage. When a $5M property is destroyed, ordinary policies fail — you need guaranteed replacement cost, scheduled fine art, and massive umbrella limits.

Luxury vacation rental insurance addresses risks that standard STR carriers simply cannot underwrite. The luxury segment of the short-term rental market is experiencing explosive growth. High-net-worth travelers are increasingly bypassing five-star hotels in favor of ultra-luxury private villas, sprawling mountain estates, and exclusive beachfront compounds.

According to AirDNA’s 2025 market analysis, the luxury STR segment (ADR above $500/night) grew by 18% year-over-year in 2024, significantly outpacing the broader market.

A luxury beachfront villa in the Florida Keys generating $1,200 per night at 65% occupancy produces over $280,000 in annual gross revenue. A high-end mountain estate in Aspen or Jackson Hole can generate $500,000 or more per year.

However, insuring a $5 million luxury STR is fundamentally different from insuring a standard $500,000 suburban Airbnb. The risks are exponentially higher, assets are bespoke and irreplaceable, and liability exposure is severe. In this guide, we explore the unique challenges of luxury vacation rental insurance and how to structure a policy that adequately protects high-value assets.

To properly protect a luxury vacation rental, investors must move beyond standard commercial markets and work with specialized High-Net-Worth (HNW) carriers.

Standard policies offer Replacement Cost Value up to the policy limit. If post-disaster inflation drives the rebuild cost beyond the limit, you pay the difference.

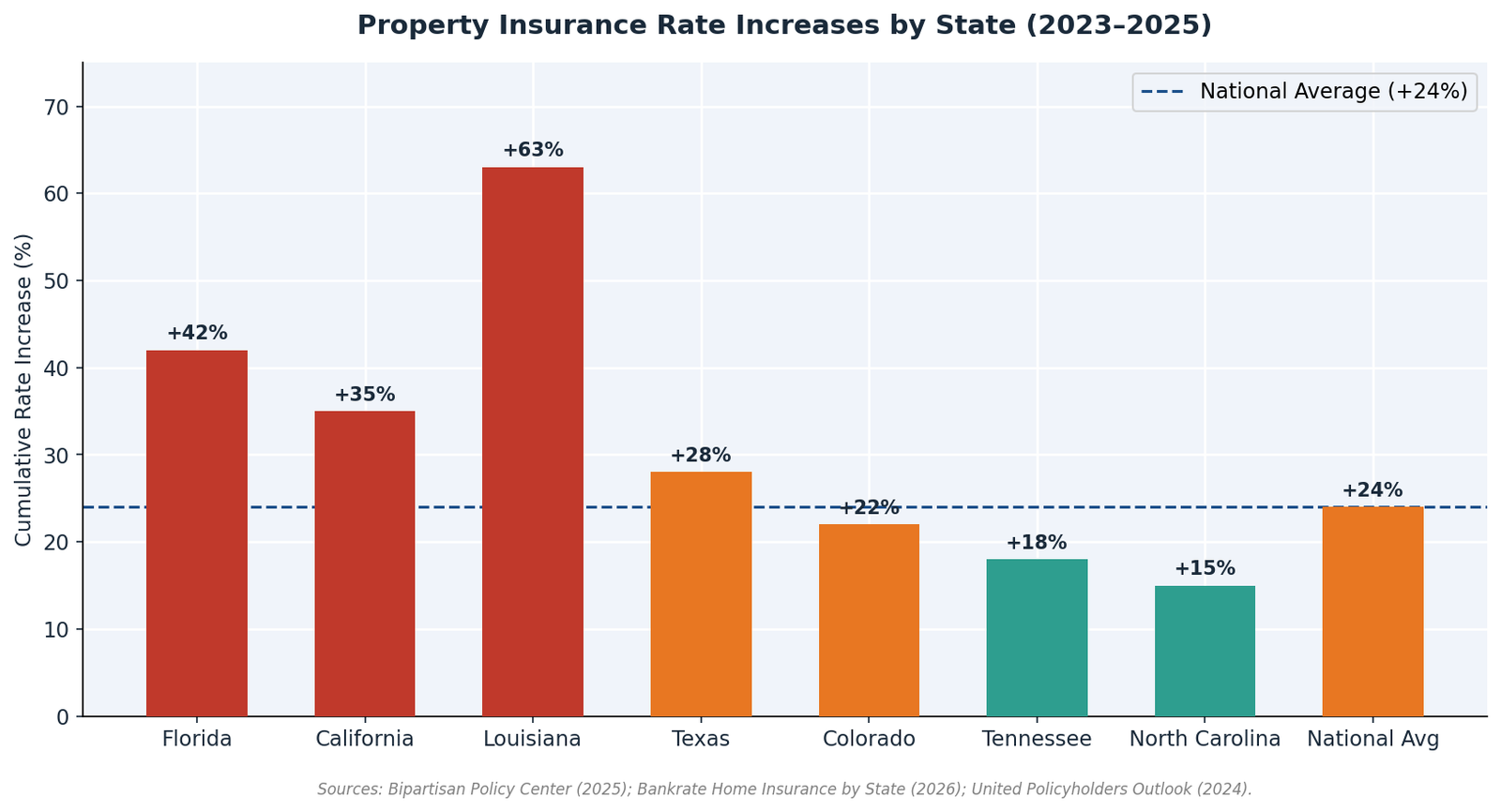

For luxury vacation rental insurance, secure Guaranteed Replacement Cost or Extended Replacement Cost (150%–200% of the policy limit). After a major hurricane or wildfire, construction costs spike dramatically. Guaranteed Replacement Cost ensures you are not underinsured.

Do not rely on a blanket “contents” limit for high-value items. Luxury policies require “scheduling” individual items via:

Luxury STR owners must secure primary commercial liability of $2M–$5M per occurrence plus a Commercial Umbrella providing $5M–$25M+ in excess coverage.

Standard commercial STR carriers are often not equipped to underwrite luxury risks. For high-value properties, investors should work with HNW specialists.

| Carrier | Specialty | Notable Feature |

|---|---|---|

| Chubb | HNW personal & commercial | Guaranteed replacement cost |

| PURE Insurance | HNW personal lines | Member-owned, exceptional claims |

| AIG Private Client | Ultra-HNW | Bespoke coverage for complex risks |

| Lloyd’s of London | Surplus lines | Covers risks standard markets decline |

| Berkley One | HNW personal lines | Strong STR endorsements |

These carriers require detailed underwriting information: professional appraisals, property inspection reports, documentation of safety systems. The process takes longer than standard markets, but the resulting policies provide far superior protection.

You cannot buy luxury vacation rental insurance online in 15 minutes. The underwriting process is rigorous, and the policy must be carefully structured.

A skilled HNW broker will conduct comprehensive risk assessment, identify coverage gaps for specific amenities (watercraft, elevators, wine cellars), structure a layered insurance program, ensure policy language satisfies lender and HOA requirements, and provide ongoing risk management advice.

The luxury short-term rental market offers unparalleled revenue potential, but it requires a sophisticated, institutional approach to risk management. A standard commercial policy is simply not designed to rebuild custom architecture, replace fine art, or defend against multi-million-dollar liability lawsuits.

For deeper context, read our companion guides on STR risk management with LLCs and the true cost of being uninsured.

Contact our private client division to design an insurance portfolio worthy of your luxury investment.