STR LLC insurance is the foundation of serious vacation rental asset protection. A single $2M lawsuit can wipe out your personal wealth — unless commercial coverage, LLC structure, and a commercial umbrella all work together.

STR LLC insurance strategy is no longer optional for serious vacation rental investors. As the short-term rental industry matures, the average host has evolved into a sophisticated portfolio operator managing multi-million-dollar assets.

According to AirDNA’s 2025 market analysis, multi-property hosts now account for over 40% of all STR listings in the United States. This professionalization demands rigorous risk management.

The average liability claim costs nearly $30,000, but severe injuries — spinal cord damage, traumatic brain injuries, drownings — can easily result in multi-million dollar judgments. Relying on platform guarantees like AirCover or a basic homeowners policy is financial negligence.

True asset protection requires a layered approach combining purpose-built commercial STR LLC insurance, legal entity structuring, and excess liability coverage. In this guide, we explore the three pillars of STR risk management.

Before diving into solutions, understand the full financial exposure of an unprotected STR investor. The table below illustrates the impact of a severe liability event across different protection levels.

| Protection Level | $2M Judgment Outcome | Personal Exposure |

|---|---|---|

| No insurance, no LLC | $2,000,000 | $2,000,000 |

| Standard homeowners only | Claim denied | $2,000,000 |

| $1M CGL, no LLC | $1M covered, $1M gap | $1,000,000 |

| $2M CGL, no LLC | $2,000,000 covered | $0 |

| $1M CGL + LLC + $3M umbrella | $2M covered (primary + umbrella) | $0 |

Adequate STR LLC insurance protection requires both the right insurance limits and the right legal structure.

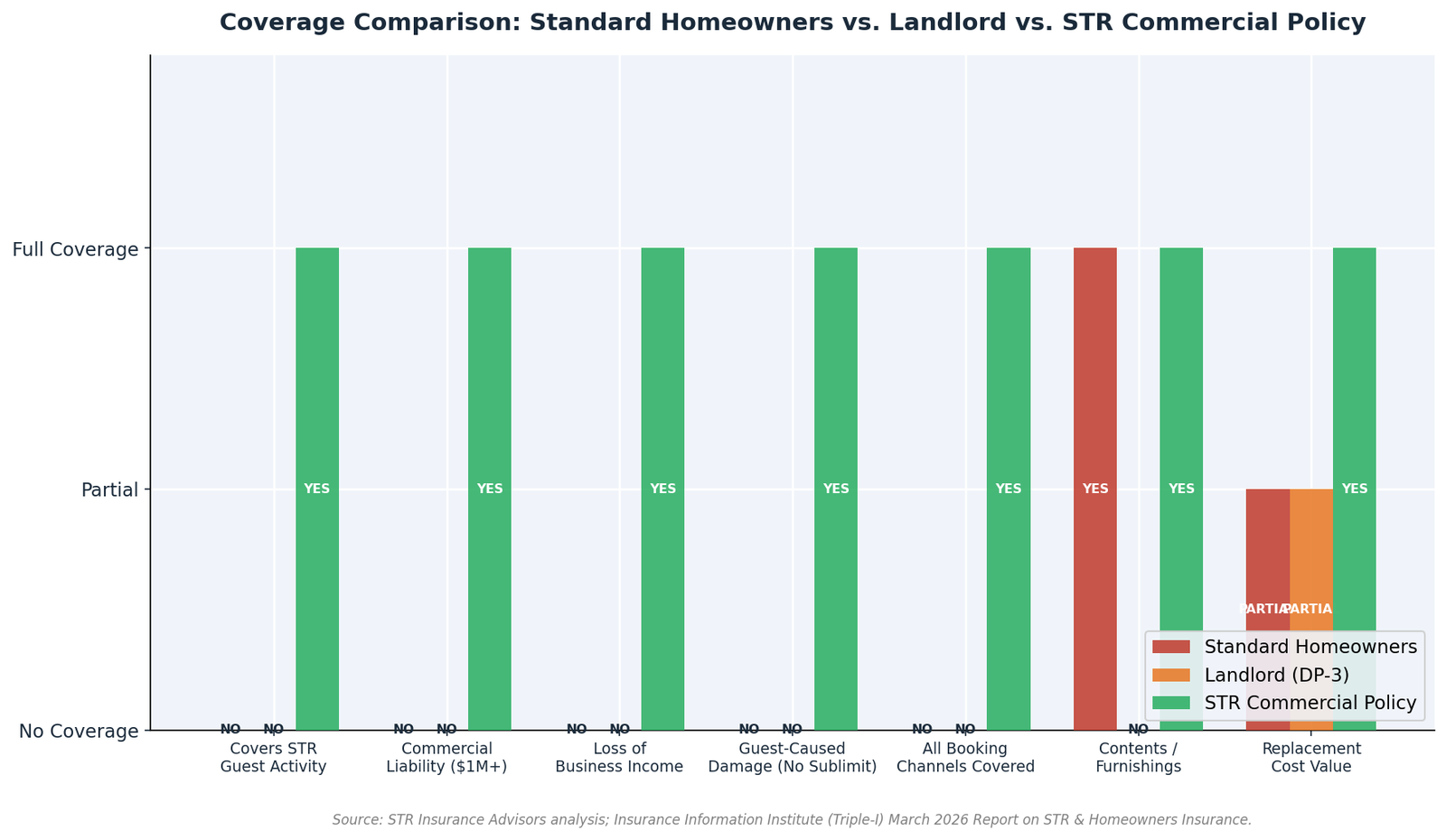

The foundation of any asset protection strategy is primary insurance. However, the type of insurance matters immensely. The Insurance Information Institute explicitly states that standard homeowners policies typically exclude business activities — any claim arising from a paying guest will likely be denied.

You must secure a Commercial Short-Term Rental Policy — not a standard homeowners policy, not a landlord policy (DP-3), and not platform guarantees.

Many investors who know they need more than a homeowners policy default to a standard landlord policy. While better than homeowners, it is still not designed for STR operations.

A purpose-built policy provides Commercial General Liability of $1M to $2M, Replacement Cost Value for dwelling and contents, no sublimits for guest damage, multi-channel coverage across all platforms, and Actual Loss Sustained income protection.

Once the primary insurance is in place, the next layer is legal separation. Many investors hold their STR properties in a Limited Liability Company (LLC).

The primary purpose of an LLC is to separate your personal assets from your business assets. If a guest is severely injured and sues, the lawsuit is directed at the LLC, not you personally.

If the judgment exceeds insurance limits, the plaintiff can generally only go after assets held within the LLC. In states with strong LLC protection laws (Wyoming, Delaware, Nevada), the corporate shield is highly effective.

An LLC is only effective if you treat it like a legitimate business. To maintain the liability shield, you must maintain a separate business bank account, sign all contracts in the LLC name, list the LLC as Named Insured on your STR LLC insurance, file all required annual reports, and never use LLC funds for personal expenses.

For investors with multiple STR properties, a Series LLC (available in Delaware, Texas, and Illinois) provides legal isolation between properties. If a guest is injured at Property A, they cannot pursue the assets of Series B, C, or D.

Traditional conventional mortgages generally require the loan to be in your personal name. Professional STR investors often use Debt-Service Coverage Ratio (DSCR) loans, which are designed to be closed in the name of an LLC.

The final layer of STR LLC insurance protection is the umbrella policy. An umbrella sits on top of your primary commercial liability limits, providing extra defense against catastrophic, multi-million dollar lawsuits.

Imagine a balcony collapses at your STR, severely injuring multiple guests. Total: $3.5 million. If your primary commercial policy has $1M limit, you are personally responsible for the remaining $2.5M. A $3M commercial umbrella absorbs that gap.

A Personal Umbrella Policy (PUP) will not cover your STR business. Because STR is commercial, a personal umbrella explicitly excludes it. You must purchase a Commercial Umbrella Policy that specifically sits over your commercial STR primary policy.

| Net Worth | Recommended Umbrella |

|---|---|

| Under $500,000 | $1,000,000 |

| $500K – $1M | $2,000,000 |

| $1M – $3M | $3M – $5M |

| $3M+ | $5M – $10M |

When properly structured, these three pillars work together to create a comprehensive protection system.

The Incident: A guest suffers a severe spinal injury at your STR and sues for $3 million.

Layer 1 — Commercial STR Insurance ($2M CGL): Your primary commercial policy immediately assigns a defense attorney. The policy pays the legal defense costs and covers the settlement up to the $2 million limit.

Layer 2 — Commercial Umbrella ($3M): Because the settlement exceeds the primary limit, your commercial umbrella activates, paying the remaining $1 million.

Layer 3 — LLC Structure: Even if the judgment was $10 million and exhausted both insurance policies, the LLC structure ensures the plaintiff cannot seize your personal home, retirement accounts, or personal savings.

Result: Your personal wealth is completely protected.

Risk management is not a place to cut corners. By layering a purpose-built commercial STR LLC insurance policy with an LLC structure and a commercial umbrella, you can scale your portfolio with confidence.

For deeper context, read our companion guides on the true cost of being uninsured and STR regulations changing insurance requirements.

We structure layered insurance and LLC programs that protect your portfolio and your personal wealth — at every claim size.